The effects of the pandemic have left us in an age of economic uncertainty and will continue to influence how we work and interact with each other on a day-to-day basis for a long time to come. The ongoing months of social distancing measures and caution surrounding our physical interactions mean that demand for the type of space we require, both personally and professionally, has changed.

Prior to the outbreak of Covid-19, McKinsey & Company reported that “over the past several years, real estate investments have generated steady cash flow and returns significantly above traditional sources of yield — such as corporate debt — with only slightly more risk.” However, in the wake of the pandemic, demand within the sector has shifted and our new behaviours are already dictating the renewed landscape of the commercial real estate market.

The winners and the losers

Industrial

With more and more consumers working from home and avoiding crowded shopping centres, there has been a remarkable increase in the popularity of online shopping.

A report from Wunderman Thompson Commerce has revealed that Amazon's share of the UK e-commerce market rose by 35% during lockdown, demonstrating Amazon’s continued traction and dominance of the e-commerce landscape.

This shift in consumer behaviour has had a knock-on effect on the real estate sector. The focus on supply chains and the growth of e-commerce has spurred greater interest in the logistics sector globally. Tritax Big Box REIT, specialising in Amazon warehouses and other logistics sites in the UK and in continental Europe, reported strong performance and growth during the first half of the year, “...there have been high levels of rent collection, stable earnings and an increase in portfolio value and rents driven by effective asset management and development activity. ”

This is a sector that has quietly been growing its footprint with strong growth, returns and even investment – taking advantage of opportunities that have arisen over the last 6 months.

Retail

Structural change in the retail sector has been ongoing for some time but as the move towards online shopping has intensified and accelerated due to Covid-19, it is seriously bad news for retail landlords and high streets across the UK. Previously core hubs of activity and commerce in towns across the country have been decimated, contributing to a growing unemployment crisis, with the likes of M&S announcing 7,000 job cuts over the next three months, and Zara planning to close up to 1,200 stores worldwide. When the situation is this challenging for huge multinational brand names, inevitably it is a bleak outlook for many local, independent stores who are being forced out of business by the increasingly challenging retail environment.

Whether or not bricks and mortar will survive from a retail perspective is a long-standing debate. The pandemic seems to have accelerated the slowly unfolding decline in our interactions with traditional retail spaces. It is a formative time for the retail sector and it remains to be seen how the balance between physical and online presence is achieved for optimal customer interaction.

Having said that, there is an area within the retail sector that has not only remained unscathed, but seems to be going from strength to strength – essentially any retail outlet that the government allowed to stay open during the strictest wave of lockdown, i.e. supermarkets, chemists and the long forgotten treasure of corner shops.

Supermarket Income REIT PLC is dedicated to investing in supermarket property and has already deployed approximately £240m of capital since late March, and is set to raise a further £150m to help with rocketing demand to help grow and sustain the reach and efficiency of the UK grocery market. They are referenced as owning “the right supermarkets in the right places” to provide a seamless service to customers regardless of whether they choose to shop in-store or online.

Offices

Is the new office, “the home office” here to stay or will we crave a return to the commuter life and the social interaction of the office, complete with mid-morning queues for a pick-me-up hit of Pret caffeine? Quite likely, we may finally achieve the Nirvana of work-life balance! Some of the largest institutions are using this time to reassess their office working policies with a clear preference towards downsizing office space and operating a rota system to attend the office 2-3 days per week. Newer companies are also realising that the prestige once assigned to a central London address achieved through flexible workspaces like a WeWork – and the consequent brand and business validation – is increasingly irrelevant and that investor money is better directed elsewhere across the business. WeWork had already taken an almighty hit in 2019 and that will inevitably continue with the cost of office space projected to fall by as much as 40% before hitting their bottom level. Covid-19 could very well be the overdue reckoning for a market correction that has been long awaited.

Leisure and hospitality

The leisure and hospitality industries have been the worst hit sector of them all. Business travel and tourism has all but been obliterated in 2020; hotels and restaurants have seen their trade decimated by travel restrictions and the prolonged lockdown with limited business hours. Smaller hotels have ceased trading and larger, well known chains have seen their business turned upside down. However, in the face of adversity comes opportunity – hotel rooms in the nation’s capital may be suffering some of the lowest occupancy rates they have ever seen but those outside London are drowning in demand from "staycationers" who are adamant they will have a holiday one way or the other.

Restaurants and bars have also suffered heavily and continue to suffer the cosmetic knee-jerk “fixes” to our, once again, rapidly growing Covid-19 rates. The decision to shut down this entire industry in totality during the first lockdown has seen many go out of business – from chains, to new concepts, to institutional family-run restaurants that are part of the fabric of the communities they were based in. Combined with the ghosts of retail spaces past, the now abandoned restaurants contribute to an increasingly bleak high street landscape. The once vibrant shopfronts and restaurant aromas have been replaced by real estate agent notices in the windows which seem to be growing by the day.

With new curfews to bars and pubs in force, this sector will continue to feel the pinch and will need to consider ways to innovate and maintain business levels to protect themselves from becoming another high street casualty and abandoned shop front.

Healthcare

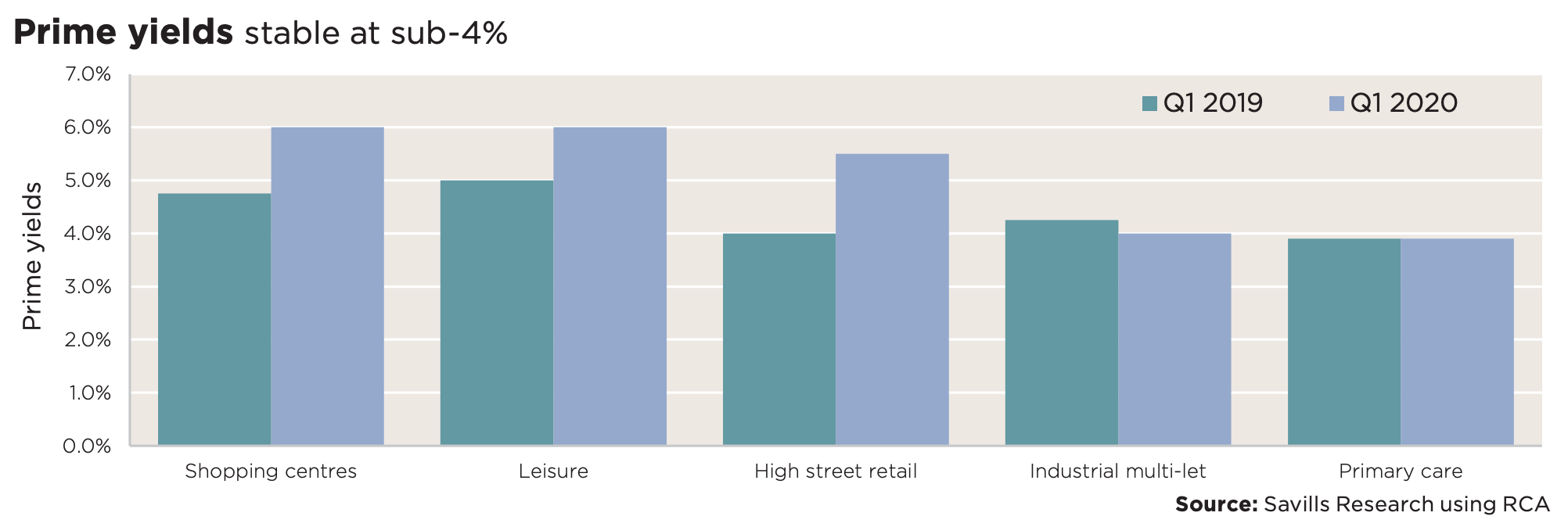

GP surgeries, dental surgeries and others falling under the ‘Primary Healthcare Facilities’ catchall have always been considered secure investments providing long term, steady income for investors as they are government backed. All of the Covid-19 related uncertainty tarnishing the rest of the real estate landscape has had the opposite effect for this particular kind of asset. RICS introduced a Material Valuation Uncertainty clause across much of the real estate market in March, but by May, this was reviewed with the first asset class having this clause removed was Primary Healthcare, which underlines its appeal and, as described by Savills “validates the attraction for investors to what is arguably the safest and most risk-averse property asset class”.

[Source: Savills]

As a tangible example, Primary Health Properties (PHP) is a £1.9bn REIT which sees 90% of its cashflow come from the NHS and HSE. In the first 6 months of the year, PHP saw its earnings grow by 29% and its rental income rocket by 20.4% and there is a feeling of confidence that this will be a continuing growth story. PHP’s Managing Director, Harry Hyman, stated “hospitals will be for acute cases and pandemic patients, non-emergency cases will visit medical centres” which will exacerbate demand for the exact type of properties that PHP invest in.

What now for Commercial Real Estate?

It is inevitable that the pandemic has had, and will continue to have, a significant impact on the commercial property sector. Whether this is positive or negative impact depends on the nature of the asset, as explored above. As expected there are losers (offices, some retail, hospitality) but, there are also winners (healthcare and retailers of essential supplies).

When considering poor investment returns and a declining real estate market, the general reaction is to think of private investors for whom most people have limited sympathy. However, there are pension funds, charities and government bodies who rely on the dividends from these investments as a lifeline.

Future success and growth will rely on thorough research, innovation and technology application. McKinsey & Company comment that, “while relatively few real estate companies were actively developing or pursuing digital and advanced analytics strategies before the pandemic, such strategies can help with tenant attraction and churn, commercial lease negotiations, asset valuation, and improved tenant experience and operations.”

There are now endless tools available for lenders, investors, landlords and developers alike to help end-end processes within this sector. Forbes note that “every aspect of our lives has become modernized, and the real estate transaction is next”. Perhaps the pandemic is the long-awaited catalyst to bring modernisation and change to a notoriously traditional industry – now could be the time for “advancements in areas, such as e-recording documents, remote online notarization (RON), e-signatures and secure online escrow deposits.”

---------------------

Shieldpay is an Escrow and Third-Party Managed Account (TPMA) service provider and works with lenders, developers, investors and lawyers to deliver a comprehensive range of payment settlement solutions throughout the commercial real estate journey. As Lenders – benefit from peace of mind through full transparency over the use of your funding. For Developers – increase efficiency and achieve streamlined project funding and onward subcontractor payments. To find out more, contact us today.

.png?width=290&name=Untitled%20design%20(1).png)

COMMENTS